How do you call an investment that failed? Answer: a long-term investment! Far too many investors think it’s a joke to stick with underperforming funds in their portfolio— selling them in favor of attractive ones— turning temporary losses into real ones.

Nothing wrong with buying and selling based on a solid plan, like when it has consistently underperformed its benchmark.

But otherwise, it’s called chasing returns, which have long cost investors gazillion amounts of money, especially when a star money manager comes along.

Cathie Wood and Ark Invest

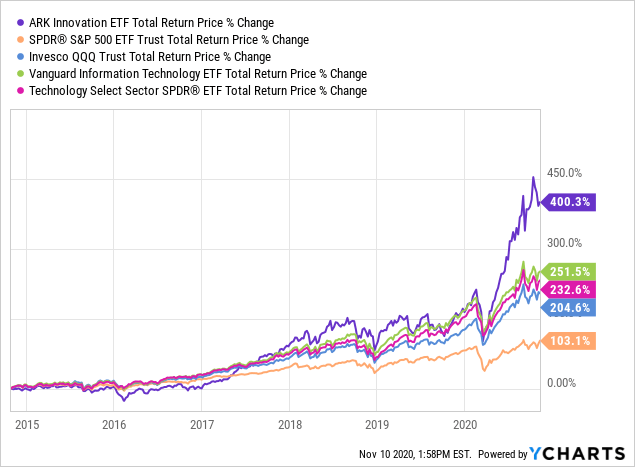

Once every blue moon, a rock star money manager emerges, kills the market and high performing indices like the FAANG stocks laden NASDAQ 100.

Her name is Catherine D. Wood, founder of Ark Investment Management, LLC. She’s famous for betting that Tesla was worth a trillion dollars in 2018 when the company appears to be on the verge of bankruptcy (TSLA market cap is currently $825 billion).

The “D” probably stands for DOMINANT because she absolutely dominated 584 funds with at least $1 billion of assets in the global equity market, crushing the likes of BlackRock and Invesco’s QQQ in the past three years. She beat 99% of them since 2014, according to data compiled by Bloomberg.

Wood’s funds focus on disruptive technologies in many exciting industries: Autonomous Tech and Robotics, Genome, Fintech, among others. As a result, investors are pouring hard-earned money into the funds as fast as they can. AUM grew from $45 million in 2014 to $50 billion today!

Suddenly, investors are salivating, and statements like, “Why am I putting up with 15% when ARKK is getting 150%?” seem to be the norm.

ARKK is definitely killing it!

That’s human nature. Because of greed and F.O.M.O., we tend to buy those that skyrocketed up. Out of fear, we sell those that went crashing down (or had average returns) without regard to the long-term outlook.

I’ve seen this “Buy High, Sell Low” movie many times before—- the ending is seldom happy.

How investors fared chasing yesterday’s superstars

I wrote about how Peter Lynch beat the market. His legendary stock-picking skill for the Fidelity Magellan Fund (FMAGX) returned a 29% annualized return from 1977 until 1990—nearly double what the S&P 500 index produced in the same period.

However, what Fidelity Investments found in their study was shocking. The average investor in the fund actually lost money because of performance chasing.

Another high-profile fund that did exceptionally well in the past is Ken Heebner’s CGM Focus (CGFMX). It even did relatively well in the 2000–2002 bear market. The stellar performance fooled a lot of investors into thinking the fund was less risky than it really was.

CNN Money had nothing but praises for Heebner:

“We may well be witnessing the most dazzling run of stock picking in mutual fund history. Since May 1998, Focus has an average annualized return of 24%, the best ten-year record of any U.S. mutual fund, compared with only 4% for Standard & Poor’s 500.”

Alas, the bear market, which ran from October 9, 2007, through March 9, 2009, crushed the fund. While the S&P 500 plunged 55.3%, CGM Focus plummeted 58.3%.

My bad experience in chasing returns

I actually owned tech-heavy QQQ as early 2003, but foolishly switched to a Janus “contrarian” fund because of the past superior returns:

JSVAX outperforms both QQQ and Russell 2000 benchmark

JSVAX is not a growth fund. But like ARKK, the fund was highly volatile— 50% of its asset was concentrated in its top 10 holdings. The largest of which was St. Joe Corporation, a company that owns vast real-estate in Florida.

Sure enough, the fund plummeted badly during the housing bust:

My money would have fared better in a CD.

After eight years, I have nothing to show for it. It would have been a different story had I simply stayed the course. Ugh!!!

Final thoughts

Choosing funds simply by looking at past returns is a big mistake. It’s like being stuck in traffic. When the other lane seems to be moving faster, it’s tempting to change lanes. But as soon as you switch, yours comes to an abrupt standstill while the one you left starts to pick up speed.

Besides compliance, there’s a reason fund prospectuses have “Past performance is no guarantee of future results” warning labels— that’s how most investors lose money. And just because an investment has done poorly recently, it doesn’t mean it couldn’t improve.

Of course, nobody knows how Cathie Wood and her disruptive approach to investing will fare in the long run. But history seems to be not on her side.

I would stick to the plan if it’s not broken.

The buying high selling low approach is what I always think of before making a decision on investing.

I may be boring, but it is better than giving someone money to underperform the market.

I’ve learned my lesson. However, I’ll always have an ear to the ground for the investments that only comes along a handful of times throughout life.

What would you consider your greatest investments made? Specific funds or companies?

I’m also a boring investor. For the first half of my career, I had crappy 401(k) investment selections. Throughout the years, they’ve probably returned less than 7% on average after the fees.

I like VGT, VHT, VIWG and had great returns owning them.

My investments with Microsoft (MSFT) and Bank of America (BAC) were both 5-baggers, but I’ve owned them a long time, and they’re less than 10% of my portfolio.

I was able to pay off my mortgage by selling BAC at precisely the right time (before the coronavirus crash). So that’s probably my best investment.

I’m not going to lie to you. The past couple of months have been nerve-wracking for us mere mortals who depend on our 401Ks to break free from the nine-to-five grind. Multiply that anxiety tenfold for someone on the brink of retirement next year like I do. It quickly became …

Scared that you might not be able to retire? Fear not! This not-so-simple calculator performs 1,000 simulations to give you valuable insight into the longevity of your savings. Of course, it’s written by no other than yours truly. So, I know exactly how it works! This is very timely because …

One of the most entertaining scenes in the movie ‘Wolf of Wall Street’ is when Mark Hanna (played by Matthew McConaughey) explains to new recruit Jordan Belford (Leonardo DiCaprio) how stockbroking business works over lunch of martini and cocaine. “F*** the clients. Your only responsibility is to put meat on …