“None of us want to pay taxes again ever!” was the last of the many demands Harry Stamper (played by Bruce Willis) and the rest of his oil-drilling crew had against the U.S. federal government in the movie Armageddon.

The 1998 science-fiction film was about a giant asteroid whose collision course will crash the Earth. The scientists at NASA plan to detonate a nuclear bomb, which must be buried 800 feet under the asteroid’s surface in order to break it apart, causing it to miss the collision with the Earth.

The government officials had no choice but to agree to their demands. He’s the best oil driller on the planet. They simply don’t want to take any chances.

As incredibly risky as the job is, it’s nevertheless one of the sweetest deals one could ever wish for: a chance to ride a shuttle to get into space, become an international hero by saving the planet, and if they happen to survive, not pay any taxes for the rest of their lives!!!

Be careful what you wish for

Do you find yourself constantly daydreaming about not paying taxes? Be careful what you wish for when you rub that magic lamp.

Or you might end up like the 60-year-old husband who instantly turned 90 after wishing for a much younger wife!

According to the Tax Policy Center (TPC), a D.C.-based firm that provides tax research and estimates, 44.5% of American households will pay zero or negative federal income tax — roughly 76.6 million households — for the 2016 calendar year.

Roughly half of this number pay no income tax because they have no taxable income. The not-so-recent news about Trump’s tax returns or billionaires’ practice of paying themselves $1 probably comes into your mind, but they are just a drop in the bucket.

They are mostly comprised of low-income households that do not pay federal income taxes. Their incomes are lower than the combination of their allowed standard deduction and exemptions, or because they receive tax credits.

Worst comes to worst, the genie might end up magically causing your present and prospective employers lay you off permanently. In this way, you don’t have to pay taxes again, ever (not even sales tax because you’d be dirt poor).

Aim to minimize taxes instead

When I say aim to minimize taxes, I didn’t mean that you should aim to get a bigger tax refund. A sizable tax refund only means that you’re loaning the government money for free.

If so, file a new W-4 form with your employer. Try this IRS withholding calculator directly from the agency itself.

17 years ago, I started preparing my own taxes. That was the last time that I aimed for a big tax refund. I got audited by the IRS instead. I was young, dumb, and stupid. Now I use TurboTax and you should too. Always, I’ll say it again, always use reliable software when filing your taxes.

Be honest with your taxes. You need to obey the taxing authority. Don’t be a crook. Crooks don’t get rich. Maybe sometimes they do, but they don’t stay wealthy. People eventually discover that they are crooks and start not to trust ’em. That’s the start of their downfall.

Minimize your income taxes

Your most powerful wealth-building arsenal is your income. I know he’s our uncle, but don’t let Sam grab a bigger slice of your earnings pie.

The following is very basic general information but I couldn’t emphasize more; tax planning is very important to conserve wealth. You need to avoid unnecessary taxes.

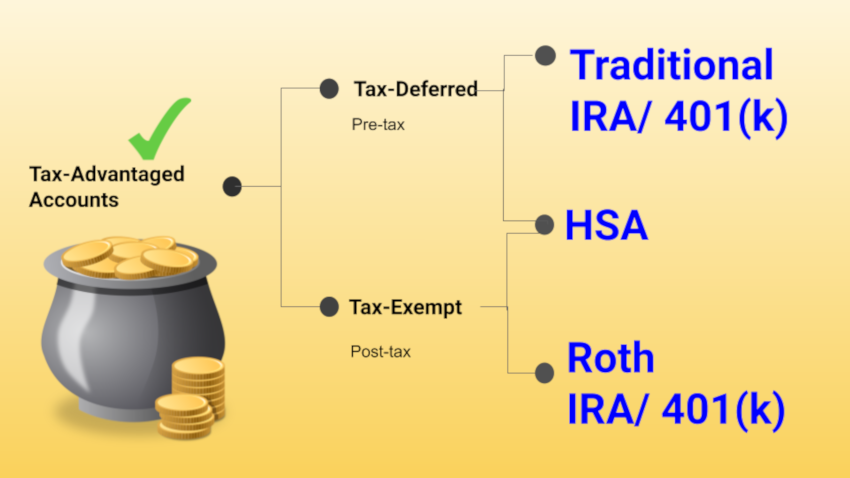

Lower your taxable income

Money contributed to an employer-sponsored retirement plan, such as a 401K, 403B, or 457, is not included in your taxable income. For these accounts, you can contribute up to $19,000 or $25,000 if you’re 50 years old or older.

If you don’t have an employer-sponsored plan, you can open a traditional IRA account and contribute up to a maximum of $6,000 this year ($7,000 if you’re 50 or older).

Roth 401K or Roth IRAs don’t have this upfront tax break because withdrawals are tax-free in retirement.

Maximize your deductions

Many of your everyday expenses can be itemized as deductions on your income tax return, saving you lots of money at tax time. However, unless you have a lot of qualifying expenses, you might be better off taking the standard deduction, as most taxpayers do. Since you can decide every year whether you want to take the standard deduction or not, careful tax planning can help you maximize your deductions in years you itemize.

Should you decide to itemize here’s some information on how to maximize them, courtesy of TurboTax

Be charitable

It also pays to be charitable. Donations to charity are tax-deductible expenses and can reduce your taxable income. Here you can find information about charitable contribution deductions.

Minimize your investment taxes

There are a number of strategies that investors can use to manage the tax bite on their investments.

Choose the right bucket to hold your investments

Use tax-sheltered accounts such as IRAs and workplace retirement plans for individual stocks you plan to hold for less than one year or actively managed funds that generate short-term capital gains. Taxable bonds and funds that invest in these types of bonds.

Taxable brokerage accounts are suitable for tax-free municipal bonds for obvious reasons. I’d also hold non-dividend-paying speculative stocks in it. In this way, you can take advantage of a tax-loss harvesting strategy, which you simply cannot do on a tax-sheltered account.

Avoid high-turnover funds or stick to index funds

Turnover means transactions, and transactions are taxable events. Unlike actively managed funds, index funds only turn over their portfolios when the companies that comprise their indexes change.

In the case of the S&P 500, a very small percentage of the companies that belong to the index change each year. This results in a very low turnover rate that translates to almost no capital gains tax.

Invest for the long haul, get a long-term capital gains rate

A long-term capital gain or loss applies to certain investments that were owned for longer than 12 months before it was sold. Long-term capital gains are assigned a lower tax rate than short-term capital gains.

I don’t consider my home as an investment, but if you recently sold your home, be aware that you may exclude up to a $250,000 gain ($500,000 if married and filing jointly) if you stayed in it for at least 2 of the last 5 years before the date of sale. In most cases, that’s zero capital gains tax!

Tax-loss harvesting

Do you have an investment that is losing capital? Selling these securities at a loss can offset capital gains tax liability. Of course, I prefer that you do not lose investment capital at all. Hold speculative individual stock investments in a taxable brokerage account.

Final Thoughts

There’s really no point in whining about taxes. What’s important is you’re doing everything legally possible to minimize them.

Besides, it’s the taxes we pay that help build the roads and bridges we use, and maintain the national or state parks we visit.

Be grateful you have the capacity to pay.

No Comments