This has been incredibly helpful. I’ve spent the last year trying to make sense of these retirement pathways. I appreciate that you’ve recommended some specific strategies to help us move forward. To be honest, I’ve been a bit unsure of how to play this game. I’ve been leaning towards strategy #3. So it’s nice to see that my initial plan is somewhat valid! Great read.

Tax-Advantaged Savings and Recommended Strategies

- By : Menard

- Category : Retirement, Taxes

Retirement

2

According to the National Study of Millionaires by Ramsey Solutions, 8 out of 10 millionaires invested in their company’s 401(k) plan, and that simple step was a key to their financial success. Not only that but 3 out of 4 of those surveyed also invested outside of company plans— mostly tax-advantaged savings!

It’s the act of regular, consistent investing over long periods that is the reason for their success. No millionaire in the study said single-stock investing was a big factor in their financial success. Single stocks didn’t even make the top three list of factors for reaching their net worth.

As a PF blogger in the “Millionaire” space, it would be foolish of me to ignore the study. Hence, I make it to the point to update this post every year especially since the SECURE ACT 2.0 has recently been signed into law.

This post, which I’ve updated for 2023, covers the most common tax-advantaged saving accounts and recommends strategies that best suit you. Hopefully, this will give you a clear direction on where to put your investments.

What is a tax-advantaged savings account?

Ordinary taxable savings or investment accounts require you to pay taxes in the year you receive your earnings— like interest on CDs, dividends on stocks, or capital gains on any investment when you sell.

Tax-advantaged accounts are different— they provide some tax benefits either by deferring or exempting taxes. The money you would have spent on taxes remains invested— your money compounds faster!

The above chart illustrates how fast $100K grows at 8% inside a tax-advantaged account compared to when it’s taxed yearly at 20%. The difference after 30 years is over $360K!

It’s no wonder experts recommend using tax-advantaged accounts to hold investments for long-term goals like retirement, health, and college savings.

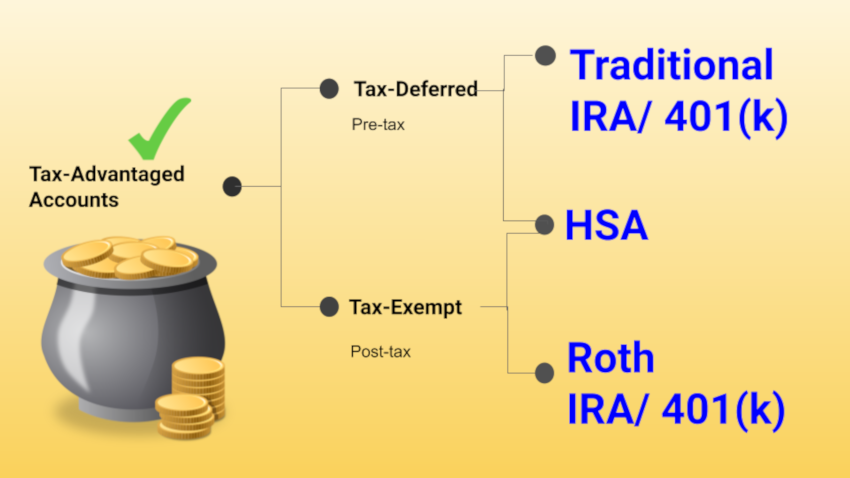

Types of tax-advantaged accounts

The names of these accounts can be confusing, but we can simplify them into two main types:

- Tax-deferred: pre-tax contributions that grow tax-deferred and that you pay ordinary income tax when you withdraw the money.

- Tax-exempt: post-tax contributions that you pay no taxes on when you withdraw the money.

All the above accounts are intended for retirement— you generally can’t access them until you’re 59 ½ or older— a 10% early withdrawal penalty will be applied on top of the tax rate on the entire distribution (or gains portion in the case of the Roth).

Health Savings Account (HSA) is the exception. You can use it to fund your present and future healthcare expenses.

I’ve included HSA because of its unique characteristic— it’s both tax-deferred and tax-exempt. Your money is not taxed on the way in, and on the way out— it’s tax-free as long as you use it for qualified medical expenses like health insurance premiums, prescription medications, and contact lenses.

IRAs or Individual Retirement Accounts, like the HSA, are personal plans— not tied to your place of employment. In contrast, 401(k) and its cousins 403(b) and 457 are employer-sponsored plans.

Note that there are many other tax-advantaged accounts like a 529 for college savings or a Solo 401(k), which also has a Roth version.

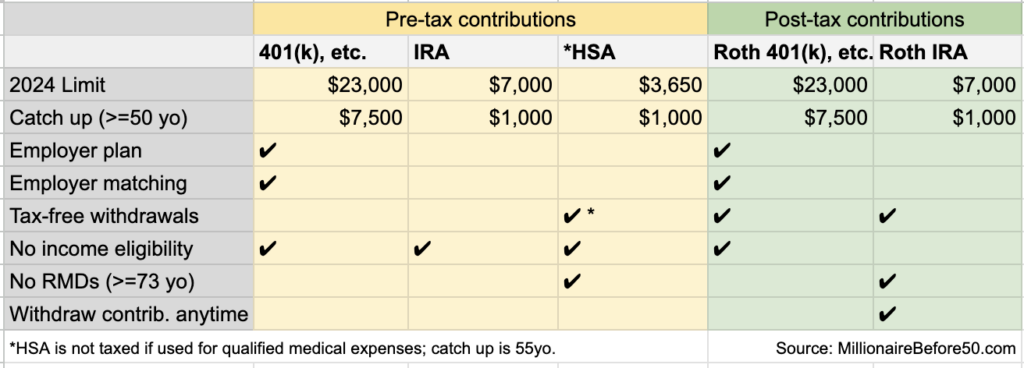

Contribution limits and other features

Each of the retirement plans mentioned above has its own rules and nuances. For example, 403(b) plans cannot accept profit sharing from their sponsor employer, which makes sense because they are intended for non-profits. 403(b) and 457 are very similar to 401(k), in many ways, like the contribution and catch-up limits.

But all these plans are just an agreement with the IRS on how they will tax you. For simplicity, I’ve created the table below to summarize the major features.

IRS contribution and withdrawal rules

The IRS won’t let you contribute to a Roth IRA when you’re single and earning under $153K or $228K for married couples. However many high-income earners find backdoor methods to take advantage of the tax-free withdrawal feature.

When you reach age 73, you’re required to withdraw a certain amount of money from your retirement accounts each year. That amount is called a required minimum distribution, or RMD.

Roth IRAs and HSAs don’t have the RMD requirement— your money can continue to compound after 73, which makes them suitable vehicles for estate planning.

With a Roth IRA, you’re allowed to withdraw your contributions at any time, which can be useful for larger emergencies like long-term unemployment.

Note that there are a variety of ways that the IRS lets you access your money without penalties before 59 ½ like when you’re buying your first home with a Traditional IRA or experiencing hardship.

Employer-sponsored plans and matching

Employer-sponsored plans like 401(k)s and their cousins have higher contribution limits— up to $22,500 in 2023. You can perform “catch-up” contributions if you’re 50 or older.

Often, employers will match your contributions up to a certain percentage to encourage you to save. For example, if your employer says they will match 50% of the first 6%— and your annual gross pay is $100K a year— you have to contribute at least $6,000 (6%) to get the full $3,000 (50%) match.

Not sure about you, but that sounds like a great deal to me!

Tax deferral reduces your taxable income.

Traditional IRAs, 401(k)s, and other tax-deferred cousins are salary reduction plans. The amount you contribute is not reported on your W-2 to the IRS, reducing your taxable income for the year.

For example, if you’re single, and you contribute $10,000 and $3,000 to your 401(k) and HSA, respectively, on a $50,000 income— you get an instant tax deduction of $13,000 for that year. Your tax bracket drops from 22% to 12%, significantly lowering your taxes for that year.

Tax exemption hedges you from future tax rates.

Roth account contributions are not tax-deductible. Hence, they won’t reduce your taxable income now, which is ideal if you’re in a lower tax bracket.

But the distributions will be tax-free if you’re in the plan for five years, and you’re 59 ½ or older at the time of withdrawal.

What’s the best contribution strategy?

Now, that I’ve painstakingly summarized the various tax-advantaged options available to you, allow me to end this post by recommending strategies that I believe most savers should follow.

For simplicity, we’ll exclude HSAs (everyone with a high income, high-deductible health plan, and in good health should maximize this). We’ll also assume that you’re not saving for kids’ college.

Lastly, we’ll assume that your 401(k)s have good investment options like the ones with broad-based low-cost index funds. Otherwise, contribute up to the match to take advantage of free money instead of maxing out.

Strategy #1: You’re convinced you will pay higher taxes when you retire.

Perhaps you already live and work in a no-income-tax state like Florida or Texas, and planning to move closer to your future grandkids in New York or California where you will build your “forever” dream home.

Or perhaps you want to tap your social security early to supplement this long-awaited European trip you plan to take quarterly.

And you’ve always been so conservative that you expect to live off high-yield bonds, annuities, and pensions you and your wife earned at work.

Lastly, you believe that AOC will someday become president and raise taxes for everyone.

Recommended strategy:

- Max out Roth 401(k) if offered at work.

- Otherwise, contribute to Traditional 401(k) up to the match, if any

- Max out your Roth IRA if you qualify.

- Max out Traditional IRA.

- Invest the rest inside a taxable account.

Strategy #2: You’re convinced you will pay lower taxes when you retire.

Perhaps you are a rockstar at work and killing it. You’re making a significant income- something you will miss when you finally leave that high-paying job.

Your kids will be all grown up (physically and emotionally), on their own, and eventually, leave the house. You have a paid-off house, or you’re likely to downsize. You have modest taste and have no dreams of living in a mansion.

And you live in a state with high-income tax rates like New York or California. But you’re planning on retiring in a tax-friendly or no-income-tax state like Florida or Texas.

Recommended strategy:

- Max out Traditional 401(k) if offered at work.

- Otherwise, max out Traditional IRA (and other pre-tax accounts).

- Max out your Roth IRA if you qualify.

- Invest your tax savings and anything extra inside a taxable account.

Strategy #3: You’re unsure if you’ll pay higher or lower taxes.

Perhaps you can’t decide what you will do or where you will live in retirement. But you want that extra security of being able to tap your Roth IRA for larger emergencies, however unlikely.

Or maybe you’re simply way too far from retirement to provide an intelligent guess.

Recommended strategy:

- Split your contributions between a Traditional 401(k) and a Roth 401(k) if both are offered at work.

- Otherwise, contribute to a Traditional 401(k) up to the match if any.

- Max out your Roth IRA if you qualify.

- Max out your Traditional IRA.

- Invest the rest inside a taxable account.