If you’re one of the smart ones who follow my blog, you’re probably aware I share our household net worth, for the past four or five years, on Labor Day. This tradition has symbolic importance.

Never mind if you have a desk job sitting comfortably in front of a computer. Loosely speaking, we are all laborers for money. If you’re not getting wealthier in the process, you’re doing it wrong. And the only way to know for sure is to track your net worth.

It’s also for transparency, accountability, and validation that the lessons I’ve been writing about work, at least for people who are walking a similar path to financial independence.

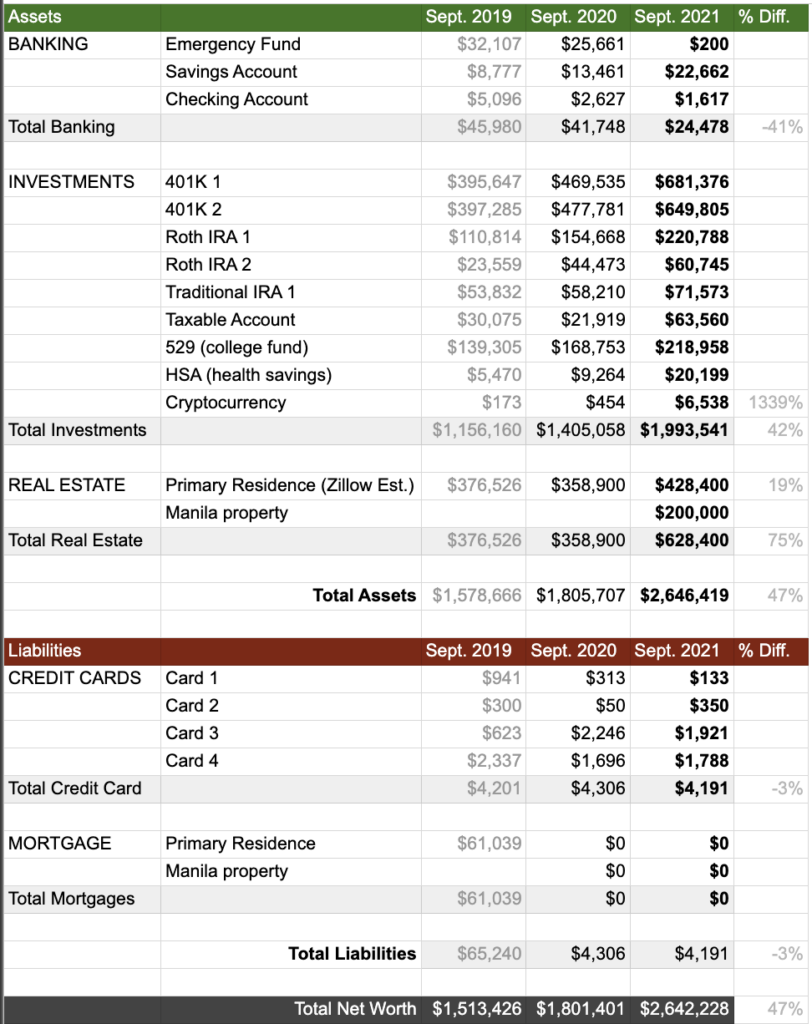

Assets are up by 47%

It has been a fantastic year for people consistently and aggressively invest in the stock market. My investment portfolio is up 42% compared to last year, including contributions. That’s because we’ve been stashing more to tax-advantaged accounts this year. The IRS starts letting you make “catch-up” contributions the year you turn 50.

Our blended portfolio mix of roughly 85/15 ratio of stock and bonds substantially beat Personal Capital’s blended mix that has a similar ratio:

Blended index is comprised of US Equities (VTI), International Equities (VEU), US Bonds (AGG), International Bonds (IGOV), and Alternatives (equal mix of VNQ/IAU/DBC).

Individual stocks helped boost our portfolio. Thanks to a couple of individual stocks that comprise about 8% of my portfolio. My two largest stock positions are Microsoft (MSFT) and Bank of America (BAC).

One that took a substantial hit is Alibaba (BABA), which has been targeted by Chinese regulators. I also own Schrodinger (SDGR), which also plummeted. So it’s not all a bed of roses.

Asset Allocation: 84% Stocks, 12% Bonds, 4% Alternatives and Cash

Take a look at the chart below, and you’ll see how our investments have steadily crept just below the $2M mark, relatively free from big stock market ups and downs.

Aaaaaah, relatively peaceful compared to last year. But for how long?

Our home value has increased 19% compared to last year. That’s according to the latest Zillow valuation. Home values have been surging across the country due to increased demand. People are scrambling to take advantage of plummeting mortgage rates that make the cost of buying a home much cheaper. The supply couldn’t keep up. It also didn’t help that lumber prices skyrocketed.

Inherited a rental property from my late mom: Frugal mom left a dozen kids in 2007 and still managed to bequest each one, including yours truly, a paid-off rental property! Located in one of the densest cities in the world— Manila, the property I inherited is worth a conservative $200K. But it could be worth as much as $300K.

Liabilities are down by 3%

We don’t have much debt to begin with. I paid off our mortgage in February last year just in time before the pandemic. And our credit cards are all being paid in full once they’re due.

On the spending front, I have to admit: I’ve been doing a lot of revenge spending this year. For example, my wife asked for a $300 portable basketball hoop for the driveway. I ended up building a $10,000 dedicated court in our backyard, which explains the big hike in July:

Expenses the past 12 months

Notice that my tiny cryptocurrency investments increased by a whopping 1339% since last year. I sold my share of Ethereum in favor of Cardano, which I firmly believe is a better investment in the long term.

Other assets not listed

Our net worth statement doesn’t include the following:

Automobiles and other personal property (< $20K): I drive a nine-year-old Toyota Prius C with 170K miles. My wife drives a 13-year-old Honda Pilot. Both actually increased their value because of the high demand for used cars. But we can both agree that they do not amount to much.

My wife’s company pension (>$250K): Pensions are hard to value. If I were to add a lump sum value, it would be at the current present value. She will receive $1,753 per month for life if she retires at 55.

All in all, net worth is up by 47%

According to a 2021 Schwab survey, Americans have revised their perspective on what it takes to be wealthy. It takes $1.9M to be wealthy, more than double the national average, but down from 2020:

Having a net worth approaching $3,000,000, I somewhat feel wealthy. But only because I no longer compare myself to others. Someone younger or smarter will always have more than you. As Mark Twain said, “Comparison is the death of joy.”

Compare yourself to where you were is the smart way to go.

Congrats! That is a huge increase in net worth. One thing I noticed with FI folks is that they don’t hold a lot of cash in comparison to their investment. That I can relate to. I do have the tendency to invest extra cash but the pandemic thought me how important it is to have emergency fund so I am saving in my Philippines and Canadian bank.

Also I learned something new: Cardano. There are so many cryptocurrency nowadays. But I am still not dipping my toes. Not yet.

I’ve realized I no longer need a big emergency fund because our house is paid off. It’s still a good idea to keep three months of expenses. I’ve reported $200 only because that’s the balance l currently have in my money market account that used to hold the fund for emergencies.

Crypto is not for everyone. You’re wise not to dip your toes when you’re not ready.

Every September 1st, I take a moment to reflect on our financial journey. What started as a simple spreadsheet in 2017 has evolved into a powerful story of discipline, strategy, and compounding returns. This year, we hit a major milestone: Net worth surpassed $4 million What fueled the climb? Staying …

Scared that you might not be able to retire? Fear not! This not-so-simple calculator performs 1,000 simulations to give you valuable insight into the longevity of your savings. Of course, it’s written by no other than yours truly. So, I know exactly how it works! This is very timely because …

I’m supposed to share our household net worth every Labor Day. It’s a tradition I’ve observed since I started this blog. Unfortunately, I got sick after my long flight from Manila. But it’s better late than never. This year, I’m going to do something different: I’m sharing actual investments! Ladies …