Investing

4

Have No Fear, Market Crashes Will Always Be Here!

While I don’t believe that a bear market is coming, one big lesson from the last two recessions is that it can’t hurt to be prepared. Crashes will always come and go. Whether it’s six months or six years from now, nobody knows. The prospect of me becoming a thousandaire …

Credit

10

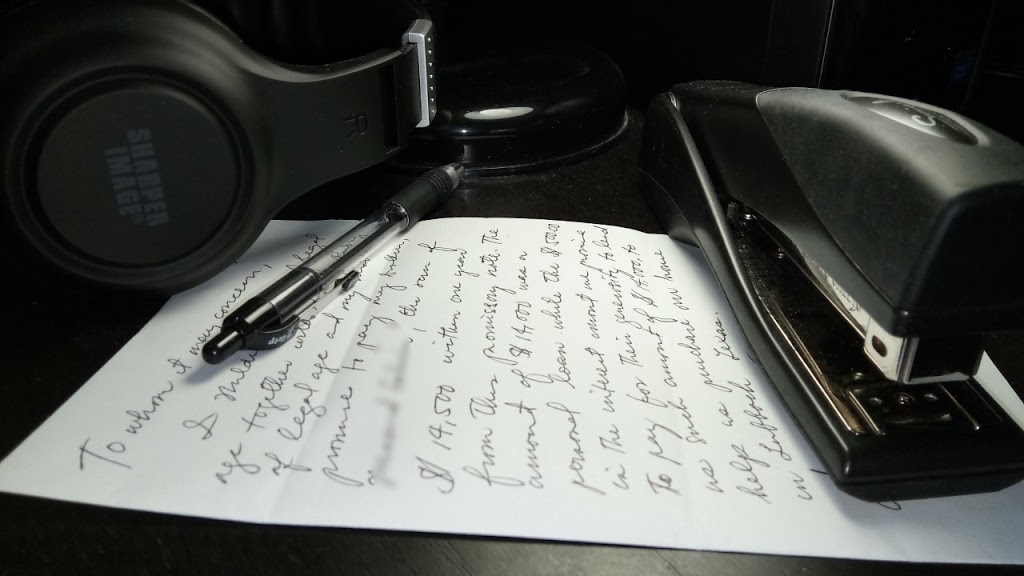

When the Lender is a Slave to the Borrower

You’ve probably heard Dave Ramsey say this many times before, “The borrower is a slave to the lender.” The quote was taken from the scriptures. That’s exactly what I had in mind when I decided to lend my sister $14,000 last summer. Finally, I can ‘enslave’ my annoying sister, who …